Latest News

New Zealand households are currently holding a record amount of their wealth in cash. Mohandeep Singh from Craigs Investment Partners notes this has the potential to be significant tailwind for our economy as more cash gets put to work.

Interest rates have had a wild ride over the past five years. Firstly, the significant cuts at the onset of COVID, followed by the sharp lift in rates as we battled to tame inflation, and then finally the easing to try and rejuvenate our weak economy.

For mortgage holders over this five-year period, the portion of their income being put towards mortgage interest payments has also moved significantly. While mortgage costs are often the first thing that come to mind when interest rates change, there’s a reasonably large ‘elephant’ which many tend to overlook.

This elephant is roughly $140b – the amount of money that New Zealand households currently have sitting in term deposits. If we add savings accounts to this equation, the number balloons to around $200b. We shouldn’t forget that changes in interest rates have a significant impact on our propensity to save, not just our willingness/ability to spend.

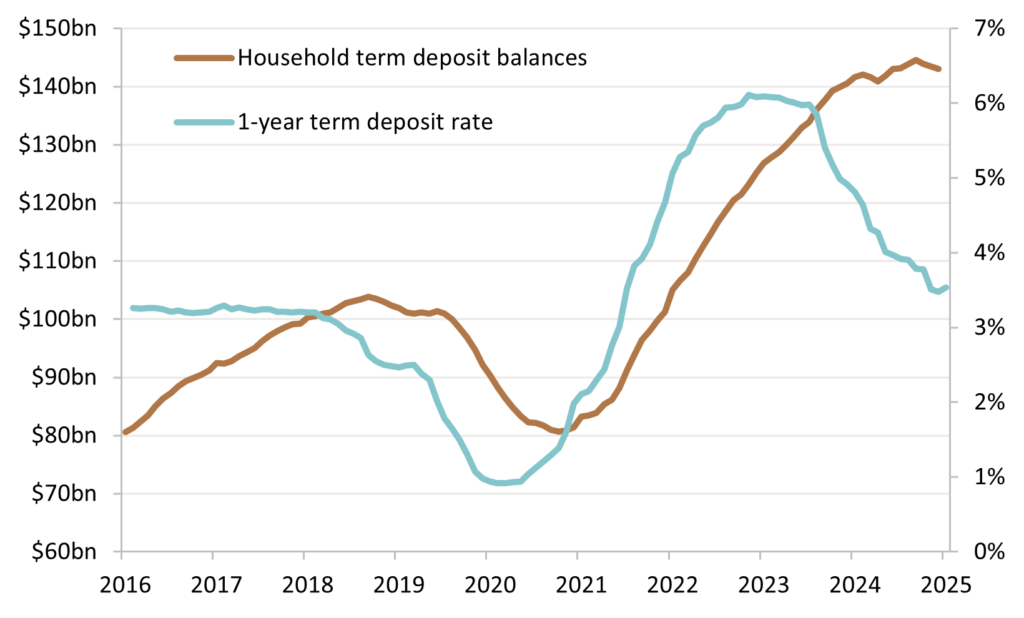

Drilling down into recent data, the relationship between the amount of money sitting in term deposits alone, putting aside savings accounts, and changes in interest rates is material.

Stepping back to 2019 (pre-COVID), Kiwi households had around $100b sitting in bank term deposits. When interest rates were cut during the initial parts of COVID, this figure fell to $80b, with many households looking elsewhere for a better return.

Change in household term deposits vs. change in term deposit rates

The following period of hot inflation saw interest rates rise rapidly. As the official cash rate stepped up, so did the attraction of term deposits which, at the peak, were offering north of 6% for a 6-month term. Consequently, plenty of households took advantage of these rates, resulting in a rise of term deposits from $80b to $140b.

Since their peak, term deposit rates have almost halved, with most banks offering around 3.5%. As term deposits roll off, and consumers are faced with the prospect of much lower returns on their cash, we expect they will look for other opportunities that offer a more attractive return.

Even if just 10% of term deposits holders decide to look elsewhere, that’s potentially $14bn dollars that will flow into productive assets, such as shares, businesses, farms and commercial property. In a small economy like ours, the magnitude of this should not be underestimated. There has been plenty made in the media about the economic benefit that will come from the ~$3bn potentially being returned to Fonterra farmers following the sale of its consumer business, and while it will be material for rural communities, the term deposit shift could be five times as big.

Additional to this potential wave of cash looking for better returns, the cost of borrowing is also coming down rapidly. This isn’t just for mortgages, but also for businesses looking to grow. There will be many businesses that have been reluctant to invest in growth due to: 1) a reasonably weak economic backdrop, and 2) the high cost of borrowing making many investment projects uneconomic. Certainly, this has been the case for some listed companies we follow.

Now the cost of borrowing has fallen, and there’s light at the end of the economic tunnel, we would expect to see an uptick in businesses investing in growth projects. This could come in the form of additional capital equipment, new/expanded premises, or new products and services. Individually, these projects or initiatives don’t need to be huge, the key is that consumers and businesses collectively have confidence in the outlook. Recent business confidence data shows a more upbeat tone from the business community in general, which should help spur growth.

While we noted that it’s not just mortgage holders that get relief, they still are a key part of the economic growth puzzle. Around two-thirds of Kiwis own a home, and around two-thirds of those homeowners have a mortgage. So around half of us have a mortgage. When mortgage rates fall, many of us benefit – but this benefit isn’t always immediate. That’s because most people typically fix interest rates for a specific period (typically one or two years). So, while the official cash rate has fallen by -3.25% (from 5.5% to 2.25%), the average benefit to households with a mortgage has only been around -1.2% to date.

Change in the OCR vs. change in average mortgage rate

This is because many are still fixed on higher rates locked in a year or two ago. As these mortgages renew onto lower rates, that reduction in the average mortgage rate paid by all New Zealand households will increase from around 1%, to closer to 2%. In a nutshell, the full benefit of falling mortgage interest rates is yet to flow through to all mortgage holders, but will gradually happen through 2026. Roughly, we’re only halfway there.

Overall, the message is simple. Firstly, changes in interest rates take time to flow through to the real economy. And secondly, falling interest rates don’t just benefit the economy because mortgage holders suddenly have more disposable cash – the economy also benefits from those with cash looking for more attractive returns. Given the amount currently sitting in cash is at record levels, it’s not hard to see the potential for this to be a significant tailwind for our economy as more cash gets put to work.

Then there’s the small matter of an election – now confirmed for 7 November. The Coalition Government has argued they’ve spent the last couple of years tightening the spending belts and getting the country’s finances back in shape. We suspect in the lead up to the election, they’ll want to demonstrate they’ve helped improve the economy and not just focused on austerity. Don’t be surprised to see more pro-growth policies in the first half of this year.

There is no doubt our economy has had a tough few years, but the scene is set for a reasonably positive 2026. Interest rates are much lower, the primary sector is in good shape, government policy is likely to be accommodative for growth, house prices have stabilised and may rise a little, and business and consumer confidence has improved. There’ll always be risks out there to worry about, but the scene is set for our economy (both locally and nationally) to stage a rebound in 2026.

Mohandeep (Mo) Singh is a Portfolio Manager at Craigs Investment Partners